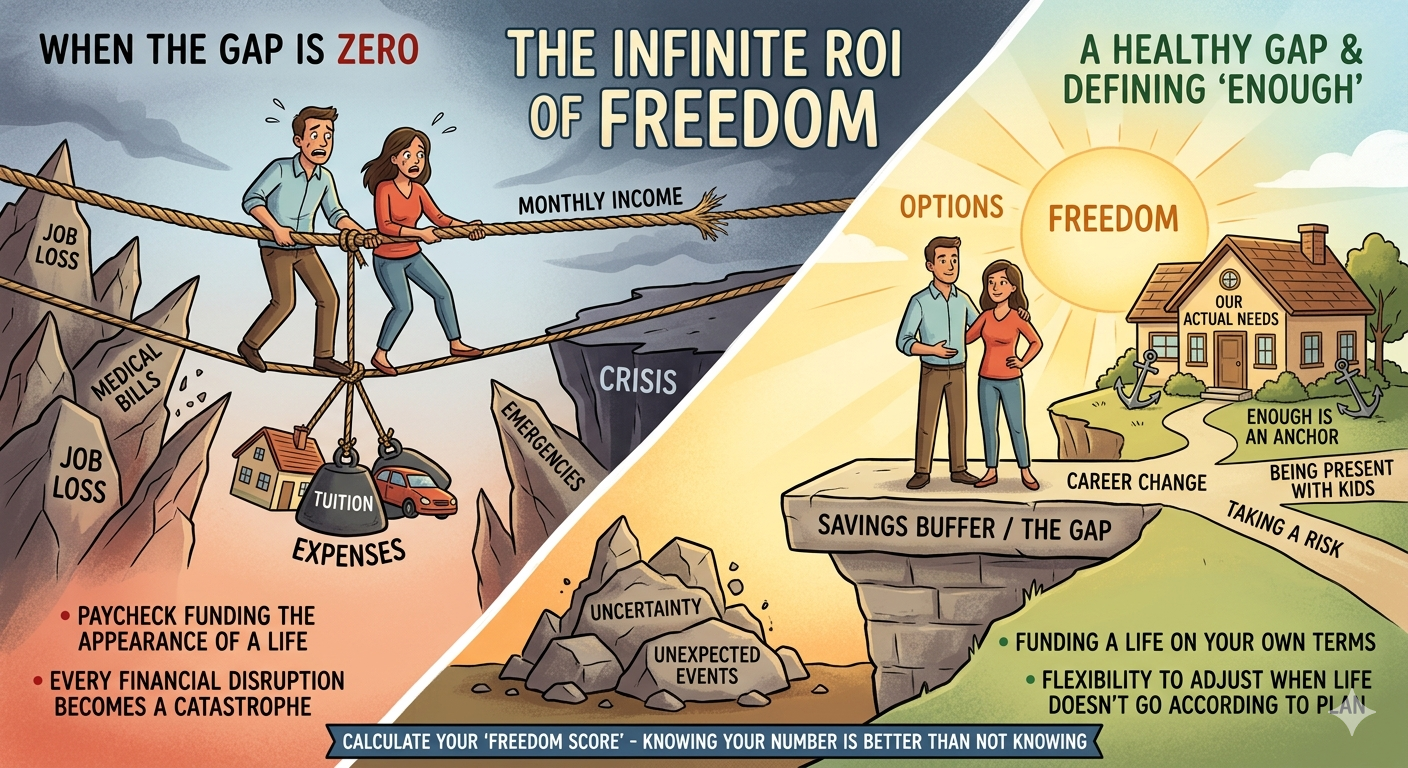

What Happens When the Gap Is Zero

There's a question, not a new one, but one that keeps resurfacing in my conversations with families.

How much is actually enough?

I know. It sounds obvious. Maybe even simple. But I'm not sure most people have actually sat down and answered it. And I think that gap, between the question and the answer, is costing families more than they realize.

I keep coming back to this trifecta of points Morgan Housel has identified, along with the question of how much is enough.

"The ability to do what you want, when you want, for as long as you want, has an infinite ROI."

"The biggest single point of failure with money is a sole reliance on a paycheck to fund short-term spending needs, with no savings to create a gap between what you think your expenses are and what they might be."

"The most important part of every plan is planning on your plan not going according to plan."

Three separate ideas. But when you read them together, they're pointing at the same thing.

The gap.

What the Gap Actually Is

The gap isn't complicated. It's the distance between what you've committed to spending and what you actually have available if your income slows, stops, or changes.

Most families don't have one. Not because they're irresponsible. Because nobody told them the gap was the thing. We spend a lot of time talking about the rate of return, investment allocation, and tax-loss harvesting. We spend almost no time discussing the buffer that makes it all matter.

When the gap is zero, every financial disruption becomes a crisis. Job loss, medical bills, a car that dies at the worst possible time. None of these is unusual. All of them happen to real people. The gap is what turns a disruption into an inconvenience instead of a catastrophe.

When the gap is healthy, you have something most people never experience: options.

The Family That Looked Fine

I worked with a family last year. Both professionals, mid-forties, two kids in the thick of their activities, combined income that most people would look at and assume everything was under control. And from the outside, it was. Nice home. Funded retirement accounts. Kids in all the right programs.

Then one of them lost their job.

Not dramatically. The company went through a reorganization. Their role was eliminated. It happens. What surprised them, and what has stayed with me, was how quickly the math changed. Because every dollar of that income had already been assigned. There was no gap. The paycheck wasn't funding a life. It was funding the appearance of one.

Within a few months, they were making decisions from a place of panic rather than clarity, which is the worst place to make financial decisions. Not because they weren't smart people, but because when the gap is zero, any disruption forces your hand.

My Version of the Same Story

I've been in a version of that situation myself, and I think about it often.

When I left my corporate career, I wasn't walking into certainty. Theresa and I weren't sitting on a number that made the decision obvious. What we had was enough of a gap that the choice was ours. Enough runway to try something. Enough space between what we needed and what we had that the risk felt manageable.

That gap didn't come from luck. It came from years of asking an uncomfortable question: what do we actually need to be okay? Not to look okay. Not to feel like we were keeping pace with everyone around us. To actually be okay, on our own terms.

That question is harder than it sounds. Because the answer requires you to be honest about what you really value versus what you've just gotten used to.

Why the Goalpost Never Stops Moving

Here's what I think is happening for a lot of families.

They hear "define enough" and assume it means scaling back, accepting less, and living smaller. That's not what it means.

Enough is a definition. It's an anchor. It's the answer to a question that, if you never ask it, makes the goalpost impossible to plant.

When you don't know what enough looks like, every raise gets absorbed. Every bonus gets spent before it arrives. Every year of progress feels like it should have produced more. Because there's no target. There's no "we made it." There's just the perpetual sense that you're almost there.

This is one of the most consistent things I see in my work with families. Not bad decisions. Not reckless spending. Just an absence of clarity about what the destination actually is.

Planning on Your Plan Not Working

The third piece of that Housel idea is the one I think gets overlooked: the most important part of every plan is planning for your plan not to go according to plan.

Financial plans are never set in stone. Life is too unpredictable, and too interesting, for any plan to survive contact with it unchanged. What changes the outcome isn't having the right predictions. It's having enough flexibility to adjust when you're wrong.

That flexibility comes from the gap.

When there's a buffer, you can absorb a bad year. You can take a risk on a career change. You can say no to an opportunity that pays well but costs you something you don't want to give up. You can make decisions from a place of choice instead of necessity.

A plan without a gap assumes everything will go right. That's not a plan. That's a wish.

The One Number to Know

If I could get every family I work with to do one thing this week, it would be this.

Calculate how many months your liquid savings would cover your living expenses if your income stopped tomorrow.

That's your gap number. That's your freedom score.

I'm not suggesting a specific target. That depends on your income, expenses, career stability, and family situation. What I'm suggesting is that you know the number because you can't have a real conversation about enough until you understand where you actually stand.

For some families, that number is higher than they expected. For others, it's a wake-up call. Either way, knowing it is better than not knowing it.

What Enough Actually Buys You

Freedom, in Housel's framing, isn't about accumulating to a specific number. It's about creating the distance between what your life costs and what you have available. That distance is what gives you options.

Options to stay in a job because you want to, not because you have to. Options to leave a job that's no longer right, even when the timing isn't perfect. Options to be fully present with your kids during a finite window of time without the constant background hum of financial anxiety.

That last one matters to me personally. The triplets are 15. Mackenzie is 13. I can count the years. And the awareness that this window is closing is one of the reasons Theresa and I revisit the question regularly. What do we actually need? What's the life we're trying to fund? What does enough look like, so we can stop running past it?

Those aren't just philosophical questions. They're the most practical financial questions you can ask.

Money is a number. Enough is a story. Make sure you're writing your own.