Your Financial Plan Is Describing a Life You Don't Live

December 9, 2010, is a date I cannot forget. That is the day my triplets were born. It is also the day I founded TAMMA Capital. One delivery room. One business launch. Same calendar square.

On that day, I had two rough plans in my head. One for the family. One for the firm. Fifteen years later, I can tell you that neither one survived contact with reality. And that is not a failure. That is the point.

Just a Collection of Short Runs

Morgan Housel wrote a few lines that have a direct tie to these life transitions:

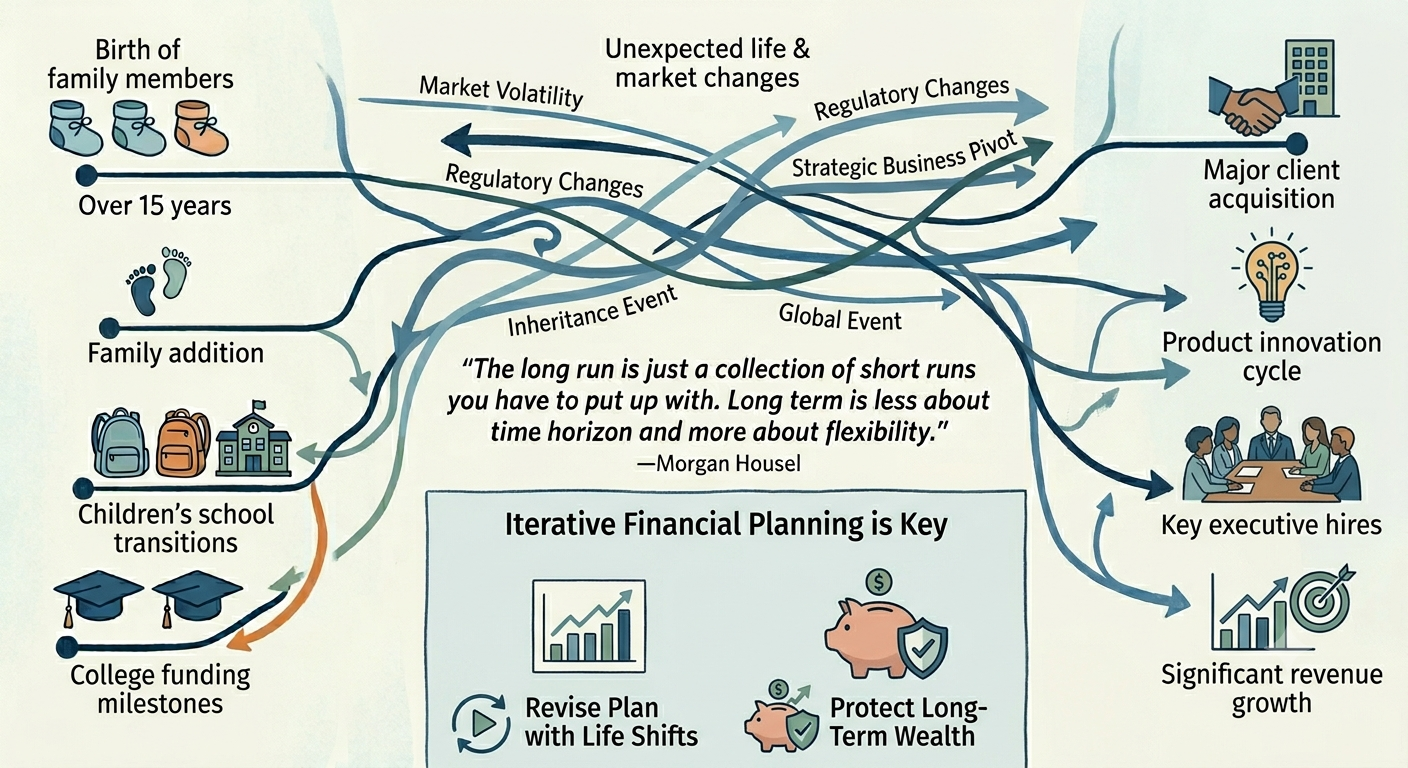

"The long run is just a collection of short runs you have to put up with. Long term is less about time horizon and more about flexibility."

That second sentence is the one I want to spend time on. Long-term is less about time horizon and more about flexibility.

If you are a Senior Manager, Director, or VP-level professional, you already know this. You just may not have applied it to your own financial life yet.

Iterative at Work, Static at Home

Think about how you treat long-term planning at the office. The five-year strategic plan does not sit untouched in a binder. It gets revised annually, sometimes even quarterly. Capital allocation gets reset after every earnings call. The talent pipeline flexes with attrition. You know that long-term plans are living documents, because you live inside one for a living.

Now think about your personal financial plan. When was the last time it was meaningfully revised? Not just rebalanced. Not just refiled at tax time. Actually, reset to match the life you live now.

If you are like most senior professionals I work with, the plan was built five years ago, possibly two promotions ago, before the equity comp ramped, before a parent got sick, before the college numbers doubled. And it has been sitting there, quietly out of date, while every other long-term plan in your life flexes weekly.

That is the conflict I want to name. Sophisticated about iteration at work. Unsophisticated about it at home. The cause is not capability. The cause is that nobody is on flexibility duty.

My Own Stack of Short Runs

Let me show you what I mean with my own count.

Day one of TAMMA, I had three newborns and a brand-new firm. Twenty-two months later, my fourth child, Mackenzie, joined us. Going from three to four kids in under two years rewrote the household spending plan, the savings rate, and the college plan. Strike one against the original plan.

Then the years moved. The triplets started high school in the past year. Madison, Aiden, and Andrew, walking into ninth grade, landed harder than I expected. Athletic fees. Travel for Madison's swim meets. The way grocery bills change when three teenagers come home hungry at the same time. None of that was modeled in the original plan.

Mackenzie joins them in high school next year. Another transition is coming, whether I have prepared for it or not. And the early college conversations with Madison have already begun. The list is forming. The cost reality is no longer theoretical.

That is at least four short runs in fifteen years inside my own family alone, without counting the business decisions that came alongside them. The original plan from December 9, 2010, cannot speak to any of it. It was written by a younger version of me who did not yet know who his kids would become.

This is not a story of failure. It is a story of how plans actually work. The plan from day one served its purpose: it got us off the starting line. It was never supposed to be the same plan five years later, much less fifteen.

A Family I Have Been Working With

Let me describe a family I will call the Hartmanns (their real name has been changed), which may feel familiar.

He is a Director of IT Operations at a health system. She is a senior product manager at an automotive Tier-1 supplier. Combined household income comfortably north of $350,000. Two kids, ages fourteen and eleven. Five years ago, they put a thoughtful financial plan in place. It accounted for college, retirement, a cash position, and an estate plan they had finally signed.

In the five years since, here is what happened. He was promoted twice and added equity compensation that he did not previously have. Her company restructured and gave her a meaningful RSU package. His mother had a stroke and now needs part-time care that may become full-time care. Their oldest's college shortlist shifted from in-state to out-of-state private schools. Their oldest also started high school last fall.

Five major transitions. Five short runs that each demanded the plan be reset.

Here is what reset looks like in practice. Their CPA filed their taxes every year. Her 401(k) was on autopilot. His ESPP vest cycle ran on its own schedule with no integration with household cash flow. Their 529 contribution rate had not moved since their oldest was nine years old. The umbrella policy was last evaluated when their net worth was roughly half what it is now. The estate documents were still in the drawer.

The plan they built was good. The plan they have today describes a family that no longer exists.

Flexibility Is a Maintenance Burden

This is the part that does not get said enough. Flexibility in financial planning is not a feature you turn on. It is not a setting. It is a maintenance burden, and that burden has to live with someone.

If your CPA only files, your 401(k) is on autopilot, your brokerage holds, and your estate documents are in a drawer, then nobody is on flexibility duty. The plan is not flexible. It is just out of date, and the cost remains invisible until something happens to make it visible. Often, that visibility shows up at the worst possible time. A bonus year that surprises you on taxes. A vest cycle that lands on the same week as a college tuition payment. A parent's illness exposes how long it has been since the estate plan was reviewed.

None of those are dramatic. None of them feels like a crisis in the moment. They are quiet, expensive, and avoidable. They compound. And by the time you look up from the daily chaos, years have passed, and you realize nobody was driving.

What to Try This Week

Get a piece of paper. Write down the last three life transitions your family went through in the past five years. Job change, promotion, equity event, health event, parent care, school change. Anything that materially shifted your reality.

Then ask yourself one question for each transition: what financial decisions in our current plan still assume we are the people we were before this happened?

That is the work. Not big-picture flexibility theory. Concrete maintenance, transition by transition. If the list is longer than you can hold in your head, that may not be a personal failing. It may be a coordination problem. And coordination problems do not solve themselves.

The Long Run Does Not Arrive All at Once

Morgan's line about the long run being a collection of short runs is the part of his quote I will keep with me longest. The long run does not arrive all at once. It shows up in pieces, year after year. Each promotion. Each diagnosis. Each kid moving up a grade. Each parent slowing down. Each one of those is a short run that asks the plan to flex.

Fifteen years in, I am still writing my own short runs. Madison, Aiden, and Andrew started high school last year. Mackenzie joins next. College conversations have already started. The plan I wrote on December 9, 2010, cannot serve any of those moments. The plan I write next year will not serve all those coming after that.

That is not a problem. That is the point. Plans are not meant to be permanent. They are meant to be lived inside and revised each time life changes the assumptions underneath them. The families who do that well end up where they intended to go. The families who don't end up somewhere else, often without realizing how they got there.

Money is a number. Enough is a story. Make sure you are writing your own.