The Settings You Configured for a Person Who Doesn't Exist Anymore

A senior director, whom I'll call Anna, came in last year with three kids, three promotions over the last decade, a husband working long hours at an automotive supplier, and a father recently diagnosed with early dementia. She wanted to know if their financial plan still made sense.

It didn't. But not for any of the reasons most articles would tell you.

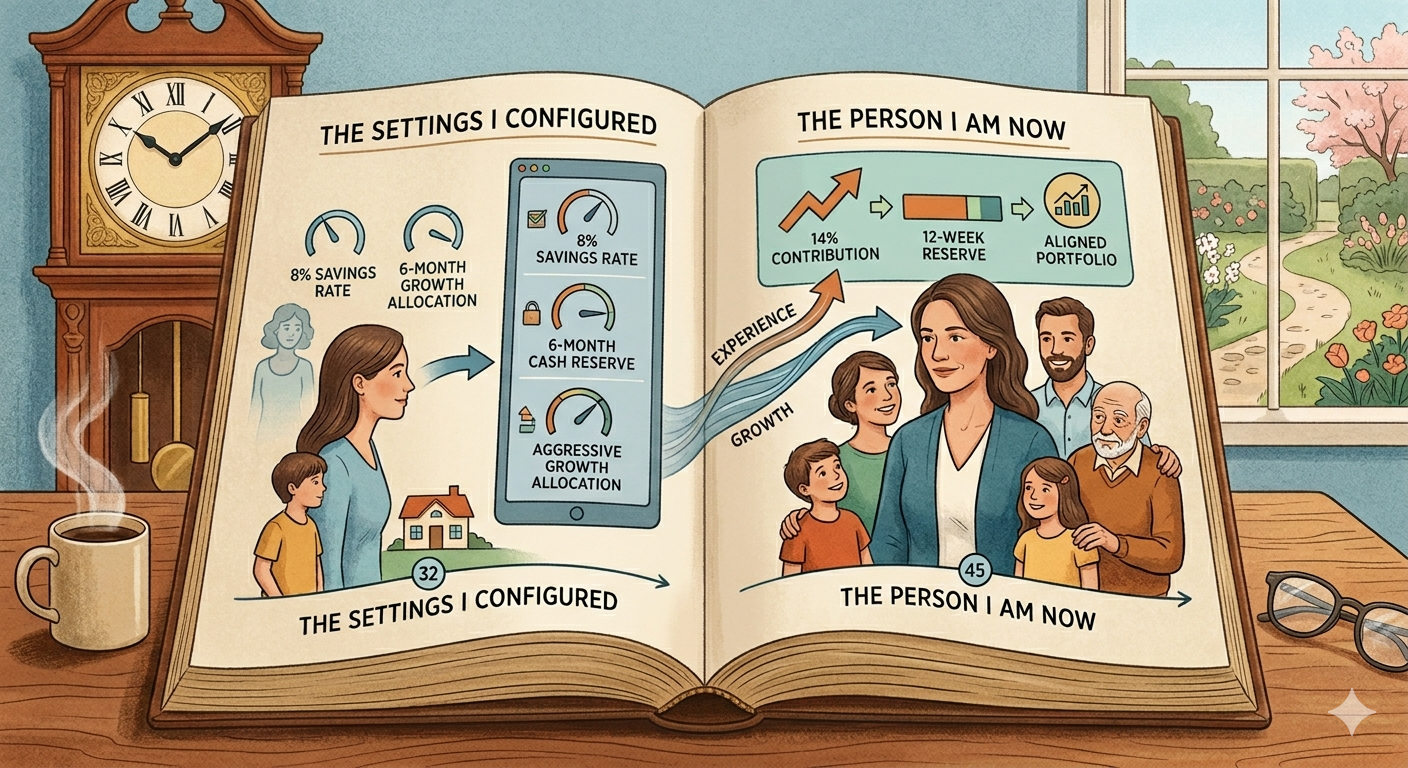

Her retirement contribution rate was 8 percent of her salary. That number had been set 11 years earlier when she was a manager, making about a third of what she makes now. She'd had three promotions in the meantime. The dollar amount kept going up because her salary did. The percentage was still for a different person.

Her cash reserves were sitting at six months of expenses. That number was set when she was a single-income household for nine months between her first and second kid. They'd been dual-income for nine years. Same target. Never revisited.

Her taxable brokerage account was in an aggressive growth allocation. That was set when she was 34, before her dad was diagnosed. She was now 45 with substantial caregiving responsibilities for two aging parents on top of three kids. Same allocation. Never revisited.

None of these settings was wrong when she made them. Everyone was right for the Anna who made them.

The problem is that Anna no longer exists.

Why This Quote Lands Harder Inward

Morgan Housel wrote something I keep coming back to. He suggested two questions you should ask in any disagreement. What have you experienced that I haven't that makes you believe what you do? And would I think about the world like you do if I experienced what you have? Then he landed the punch: “disagreement has less to do with what people know and more to do with what they've experienced.”

Most people apply this to politics or to disagreements with someone else. I want to apply it differently. I want to apply it inside you, between the version of you who set up your financial life and the version of you sitting here now.

Because for most senior professionals I work with, those two versions of you are in a disagreement they don't know they're having. The 32-year-old version of you set up your savings rate, reserve target, allocation, insurance, cost-splitting with your spouse, and assumptions about debt. Those settings were right for the experience you'd had at the time.

Then you lived through another fifteen years of experience that should have rewritten them. Promotions. Kids. Aging parents. Industry changes. Health events. A spouse going back to work. A spouse stopping work. None of it makes it into the settings unless you actively go back and rewrite. And almost nobody does.

Why It Stays Stuck

Here's what I've watched happen in this exact pattern over and over.

The 32-year-old version of you set those defaults with conviction. You did your research. You read the books. You picked numbers that felt right. The decisions were grounded in your real experience at the time. And then you went on with your life, and those settings became invisible. They moved from active decisions to background defaults.

Defaults don't get reconsidered. They get inherited. You inherited them from yourself. And the longer they sit there, the more they feel like facts of nature instead of choices you once made.

Anna didn't think of her 8 percent contribution rate as a decision she'd made. She thought of it as just what she contributes. The frame had hardened. The choice had disappeared.

What I Know From the Other Side of Thirteen Years of Moving

I grew up in one house. My parents still live in it. For the first 22 years of my life, I was rooted in one place. Then I started my career and lived in five different states over the next thirteen years. Ten moves. Boxes into apartments and houses, I knew I wouldn't be in long. Then Theresa and I landed in Commerce Township, and now it has been fifteen years and counting. Three distinct chapters. Three different sets of beliefs about what roots are worth.

At 30, I believed roots were a luxury you couldn't afford if you wanted a career. I'd watched what happened to people who stayed too long, who passed on a relocation, who got attached. I kept things liquid. I didn't get attached to a neighborhood or a friend group, because I was going to be moving again in 18 months. That was the right advice for a rootless career.

At 50, I believe roots are the whole point. Over the last fifteen years here, neighbors became family. The parents I see every week at our kids' sporting events became family. Parents I know through school events became family. It happened slowly and then all at once. I didn't plan for it. I wouldn't have predicted it at 30.

The same thing has happened at TAMMA. Clients become friends. Friends become family. That makes it emotionally harder when someone moves away or decides to go a different direction in their life. I would rather be connected like that than be someone's, quote, financial advisor and nothing more. It is the same person doing the work. A different belief about what the work is for. A different experience built it.

And yet. The 30-year-old instincts still fire. I'll notice myself hedging on something, holding back on a longer-term commitment, treating a decision as more reversible than it actually is. The voice in my head making those calls is still the voice that lived in five different states. He earned his opinions. He's no longer the version of me running life.

If I'm honest, this is part of why the conversations I have with my own clients land the way they do. I'm not lecturing from above. I'm telling you something I've watched myself do.

The Spouse Layer

There's a second version of this that I see in nearly every dual-income household I work with. It's not just that one of you is running on outdated personal settings. It's that the two of you formed your financial beliefs at different times, from different experiences, and you've never actually compared notes.

One spouse formed their core beliefs during a year their parent was unemployed. The other formed theirs during a year their family did a major renovation. Both are now 47, both senior in their careers, both convinced their own instincts are the right ones for the family. They think they're disagreeing about facts. They are not. They are arguing on behalf of two different 25-year-olds, neither of whom has been in for twenty years.

The fastest way through that argument is not a spreadsheet. It is naming what's happening. Once you can both see that you're each defending a version of yourselves that no longer exists, the actual decision in front of you gets easier.

A Ten-Minute Audit

Here is what I'd like you to do this week if you can find ten minutes. You can do it standing in your kitchen.

Pick one financial habit you've held for more than five years. Your savings rate. Your cash reserve target. Your investment allocation. Your insurance coverage. Your debt strategy. Whatever it is, pick one and write it down.

Then ask three questions. When did I form this? What was true about my life at that moment? What has changed since then that should have updated it?

If the answer to the third question is meaningful, and you haven't actually updated the habit, you've found something worth fixing.

Most senior professionals find at least two of these in a quick check. Not because anything is broken. Because life moved, and the settings didn't move with it.

Where Anna Landed

Anna walked out of our second meeting having raised her contribution rate to 14 percent, reduced her cash reserves to twelve weeks of expenses, and reallocated the brokerage account to something more aligned with the responsibilities she actually carries today. None of those changes was complicated. They had just been waiting for someone to tell her the defaults were still working for the 34-year-old version of her.

Her financial plan didn't get more sophisticated. It got more current.

That's the thing nobody tells you when you set up a financial life at 30. You're not setting it once. You're starting a conversation with yourself that needs to happen again every few years, because the person living the plan keeps changing, whether you do anything about it or not.

Money is a number. Enough is a story. Make sure you're writing your own.