The Expectation Gap

What if the reason so many people feel financially anxious, not broke, not careless, just vaguely unsatisfied, has almost nothing to do with their actual financial situation?

What if it's the scoreboard?

Charlie Munger, near the very end of his life, was asked what his secret was to living so happily at 98. His answer was brief and a little startling. He said the first rule of a happy life is reasonable expectations. Not hustle harder. Not compound interest. Not finding your passion. Reasonable expectations.

"If you have unrealistic expectations, you're going to be miserable your whole life. You want to have reasonable expectations and take life's results good and bad, as they happen with a certain amount of stoicism."

I've been sitting with that this week. Because in 20-plus years of working with families, and in my own life, this is one of the most consistent things I see. The suffering isn't usually from what people don't have. It's from the gap between what they have and what they assumed they'd have by now.

The Scoreboard Nobody Chose

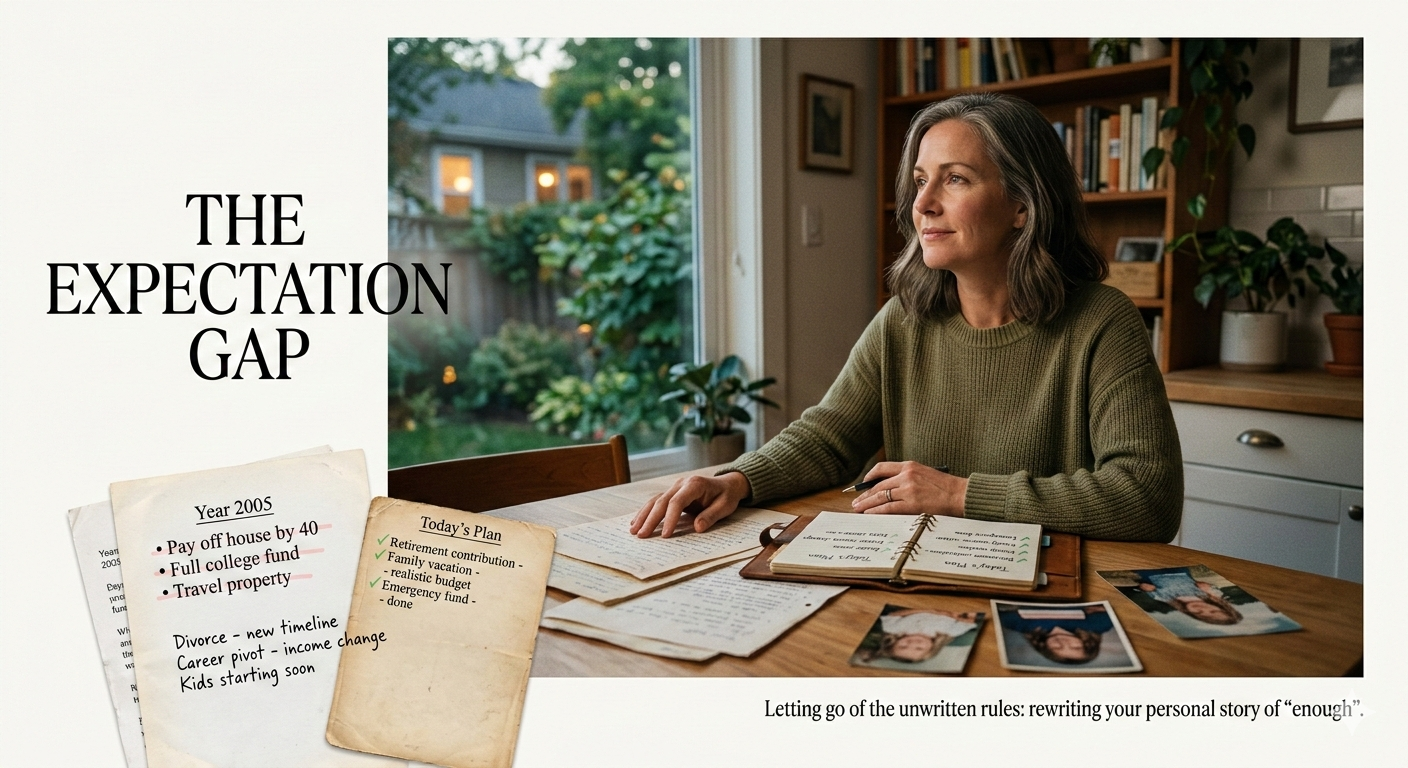

I had a client I'll call Sandra. She's in her mid-40s, has two kids, a solid career, no debt outside of her mortgage, and a real savings rate. By most metrics, she's doing well.

But she'd come in for a conversation and felt deflated. Not panicked — just flat. And it took me more than a few minutes to figure out what was underneath it.

It turned out Sandra had a very specific picture of what 45 was supposed to look like. Mortgage paid down to almost nothing. College accounts are fully funded. A vacation property somewhere warm. A portfolio big enough that retirement felt certain, not theoretical.

She'd constructed that picture in her late 20s, early 30s, when the future felt like something she could engineer. And then life happened. A career pivot. A divorce. Several years of solo parenting. None of it catastrophic. Just life doing what life does.

By the time we sat down, the picture didn't match reality, even though the reality was genuinely good.

The problem wasn't her financial plan. The problem was the invisible scoreboard she was still playing against, one she'd built at 28 and never questioned.

I recognize this because I live it too. Theresa and I have four kids: triplets who are 15, and our youngest, who is 13. We've been in full-contact parenting mode for years. And there are moments where I catch myself measuring our life against some version of where I thought we'd be at this age. The business. The retirement accounts. The pace of everything.

It's a fast way to feel behind. Even when you're not.

What Munger Actually Meant

Munger wasn't telling anyone to stop having goals. He wasn't advocating for passivity or low ambition. He was making a more precise point about where expectations come from and whether we've ever examined them.

There's a difference between a goal you've chosen, one that's anchored to what you actually value, and an expectation that arrived quietly from your parents, your peers, your neighborhood, or some magazine article you read at 30. Most people have both, and they've never separated them.

The goal you chose is useful. It gives you direction. You can adjust it when the world changes.

The expectation you inherited is different. It just sits there, comparing your life to a picture you didn't really paint, generating a low-grade sense of not enough.

Things You Can Control

Munger's second point is the one that gets lost: stoicism. He said to take life's results, good and bad, as they happen with a certain amount of stoicism.

This word gets misread. People hear it and think it means going through life emotionally flat, not caring, not feeling, just grinding forward. That's not it.

Stoicism is the practice of not letting things outside your control run the show inside your head. You feel the thing. The market drops. The deal falls through. The year doesn't go the way you planned. You feel it, and then you decide what to do next rather than getting swallowed by it.

In my work with families, I see the opposite constantly. A rough quarter, and someone wants to blow up a ten-year plan. A bonus that doesn't arrive, and someone feels like a failure. A house that doesn't appreciate the way they thought it would, and suddenly the whole financial picture seems wrong.

None of those reactions help. And underneath most of them is an unexamined expectation, a story about what should have happened by now.

The Families Who Seem Actually Settled

Over two decades of working with families, I've noticed something about the families who seem genuinely at peace with where they are, not just financially stable, but actually settled.

They've done the work, sometimes intentional and sometimes just through accumulated hard experience, to separate the inherited scoreboard from the one they actually want to play on.

They still have objectives. They're still working toward things. But they've gotten clearer about which targets they chose and which ones just showed up. And they've gotten better at not treating every deviation from the plan as a referendum on their worth.

A couple I work with has two adult kids, both in their early 60s, went through a period a few years ago where they had to significantly rework their retirement timeline. A business setback. Unexpected medical costs. The kind of thing that would have, at an earlier point in their lives, felt catastrophic.

Instead, we sat down, adjusted the plan, and kept going. Not because they didn't feel it, they most certainly did. But because they'd done enough work on the expectation side, the adjustment didn't feel like a failure. It just felt like life.

That's what Munger was pointing at. Not low standards. Calibrated ones.

The Expectation Audit

There's a version of financial planning that's purely mechanical. You set objectives, build projections, manage the variables, and adjust when needed. That part matters. But it's a fraction of the picture.

The bigger part is the story you're telling yourself about what this was all supposed to look like. And that story is often invisible, running in the background, generating a quiet sense of not-quite-enough, even when the numbers are fine.

Purpose doesn't change. Objectives do. That's something I say a lot in my practice. What you're actually trying to build, the time with your family, the freedom to choose your work, the ability to help your kids get started, that tends to be pretty stable. But the specific numbers attached to it? Those are negotiable. More negotiable than most people allow.

The Action Step

This week, try something small. Pick one area of your financial life where you feel behind, where there's a low-grade sense of not enough or not there yet.

And ask: where did that expectation come from?

Not the goal — the expectation. The picture you built of what this was supposed to look like. Did you choose it? Or did it arrive from somewhere else — a parent's voice, a peer's lifestyle, a version of yourself from 15 years ago that had the whole thing figured out?

You don't need to fix it today. You don't need to throw the whole thing out. Just notice where it came from.

Because you can't rewrite a story you haven't read yet.

Money is a number. Enough is a story. Make sure you're writing your own.