Why Stories Move Us More Than Numbers

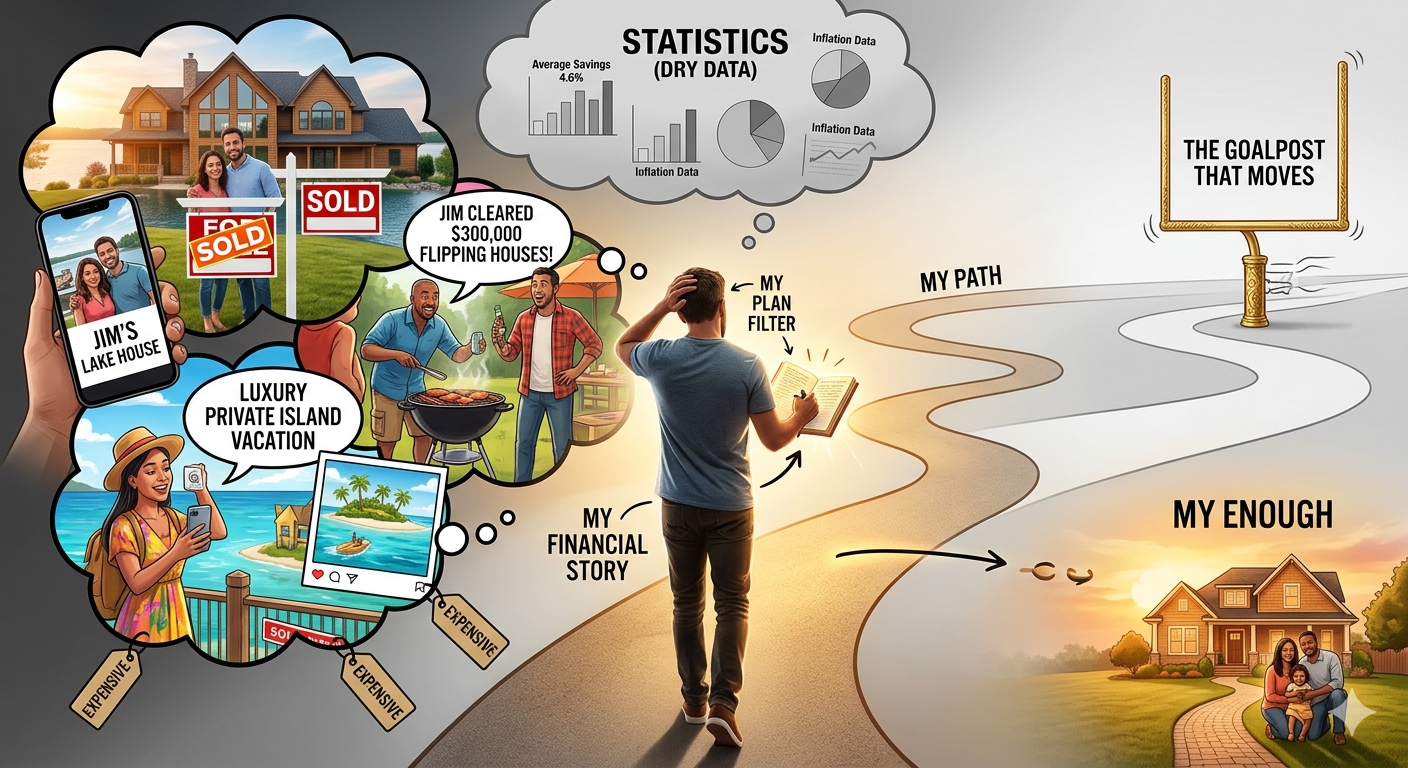

Nobody has ever changed their financial plan because of a pie chart.

I mean that seriously. In twenty-plus years of working with families, I have never once had someone walk into my office and say, "Paul, I saw a chart showing that the average American household saves 4.6% of their income, and that really shook me." That has never happened. Not once.

But I have had dozens of families walk in rattled because a friend just bought a bigger house. Or a coworker mentioned she maxed out her 401(k) by March. Or a cousin posted photos from a vacation that looked like it cost more than some people's cars.

Those aren't statistics. They're stories. And stories are what actually move us.

Morgan Housel captured this well when he wrote: "Stories are more powerful than statistics because they take less effort for your brain to contextualize complex issues." He used the example of housing. You can cite data showing that home prices relative to median incomes are above their historic average. That's accurate and useful. But it doesn't hit you in the gut the way hearing that your buddy Jim just cleared $300,000 flipping houses does. Jim's story gets retold at barbecues. The statistic gets forgotten before the sentence ends.

And this is the thing I keep coming back to in my work with families at TAMMA. The numbers almost never cause the anxiety. The stories do.

The Story That Rewrote the Plan

Last year, a couple came in for their annual review. Dual-income household. Three kids. Solid retirement trajectory. Emergency fund in place. College savings on track. By the numbers, they were doing exactly what they needed to be doing.

But the husband was agitated. Not about their portfolio. About a lake house.

His college roommate had just posted about buying one. Photos of the dock, the sunset, the kids running through the yard. The caption was something about "finally making it." And that post had been living rent-free in this guy's head for weeks.

We pulled up his plan. Nothing had changed. His numbers were still strong. His trajectory was still solid. But the story of his friend's lake house had rewritten his internal definition of enough. What had felt like progress two months earlier now felt like falling behind.

That's the power of story over statistics. A data point about vacation home ownership rates wouldn't have moved him at all. But one friend's Instagram post rewired his entire sense of where he stood.

Stories Are Contagious. Data Is Not

I think about this in terms of how information actually spreads in our lives. When was the last time you overheard someone at a kids' soccer game citing the national average for 529 plan contributions? Never. That doesn't happen.

But parents talk about what other families are doing all the time. Who's renovating their kitchen. Who just leased a new car. Who's going to Europe this summer. Who pulled their kid out of public school and put them in private. These are stories, and they travel fast because our brains process them effortlessly. No mental lifting required. You hear it, you picture it, you feel it.

Statistics require work. You have to understand context. You have to interpret what "mean reversion" means and why it matters. You have to fight the urge to skip ahead to the conclusion. Stories skip all of that. They go straight to the emotional core.

Housel's point is that this asymmetry is dangerous. If enough people believe something is true because they keep hearing the same stories, unsustainable ideas can gain durable life support. Think about the housing bubble. It wasn't sustained by data. Stories sustained it. By Jim, who made $300,000. By neighbors who refinanced and took cash out. By the collective narrative that real estate always goes up. The data said otherwise. The stories won, until they didn't.

The Stories Running Your Financial Life

Theresa and I are not above this. I want to be clear about that. I told you about the mom on the sideline at the triplets' game who left her corporate job to be present. I stood there doing math in my head for ninety seconds, comparing her number to ours. Wondering if we could restructure something. Her story was about the one thing busy parents want most, time, and it almost had me questioning a plan that was working perfectly well. The story tries to override the intention. Every single time.

But here's what I've learned working with families across generations, because I work with clients, their adult children, and their parents. The families who end up in the best position, both financially and emotionally, are the ones who learn to recognize when someone else's story is trying to hijack their plan.

They don't ignore stories entirely. That's not realistic. We're human. But they develop a filter. They hear the story and ask: "Is this relevant to my life?" Does this change anything about what we've decided matters? Or is this just noise that feels important because it came packaged as a narrative instead of a number?

The families who struggle are the ones who keep absorbing stories without that filter. They hear about Jim's house flip and suddenly they want to flip houses. They see the lake house post, and suddenly their perfectly good vacation plans feel inadequate. They're living in a constant state of reaction to other people's narratives, and it's exhausting.

Writing Your Own Story

I think the antidote isn't better data. It's a better story. Your own story.

When I sit down with families, what we're really doing isn't just running numbers. We're building a narrative. A story about what this family values, what they're building toward, and what enough actually looks like for them. Not for Jim. Not for the lake house guy. For them.

Because if you don't have your own story clearly defined, you'll keep borrowing someone else's. And borrowed stories are expensive. They lead to decisions that don't fit your actual life. They push the goalpost in directions that have nothing to do with your purpose. They create a version of success that isn't yours and then make you feel like a failure for not reaching it.

One of the hardest things in life is to get the goalpost to stop moving. Stories are what keep pushing it. Not market returns. Not inflation data. Not tax law changes. Stories about what other people are doing, having, and achieving.

The statistics of your financial life might be perfectly sound. Your savings rate may be healthy. Your debt is manageable. Your portfolio is growing. But if the story you're telling yourself is that it's not enough because of what you see other people doing, the statistics don't matter. The story wins.

Your Action Step

This week, I want you to try something simple. Pay attention to the financial stories that get into your head. Not data. Not headlines about the Fed or interest rates. The personal stories. The thing your coworker said. The post you scrolled past. The conversation at the dinner table.

When one lands, ask yourself: Is this my story? Or is this someone else's story that's trying to rewrite my plan?

That single question can save you from a decision you'd regret.

Because money is a number. Enough is a story. Make sure you're writing your own.