The Greatest Story Ever Told

I want to ask you something, and I want you to sit with it for a second before you move on.

If someone looked at your last three months of bank and credit card statements, no judgment, no context, what story would they tell about you?

Not about your income. Not your savings rate or your investment allocation. Just the spending. What you actually bought, week after week.

Would that story match what you'd say out loud if someone asked what matters most to you?

For most people, the answer is: not entirely.

"There's a science to spending money — how to find a bargain, how to make a budget. But there's also an art to spending. A part that can't be quantified and varies person to person. How people spend is far more visible — so what it shows about who you are can be even more insightful."

Morgan Housel calls money 'the greatest show on earth' because of what it reveals. Not because spending is always rational, he says that too, it's personal, it's messy, it's emotional. But even the irrational parts are telling you something.

The Science Is Not the Hard Part

The science of money matters. Knowing how to compare prices, how to build a plan, and how to set up automated savings, that's real, and it works. If you haven't done the basics, start there.

But here's what I've noticed after years of working with busy families: most people who come to me aren't struggling with the science. They know they should save more. They know the subscriptions are adding up. They know they could probably cut back on food delivery.

The harder problem is the art.

The art is asking what's behind the spending. What's driving it? What story it's quietly telling and whether that's the story you actually want to be in.

What I've Seen in Client Households

I had a couple come in a while back, I'll call them Diane and Steve. Two kids, a third on the way, both working, good income, solid retirement contributions. They came in thinking their investment returns were the problem.

When we pulled their spending, it wasn't catastrophic. But it was revealing. A significant portion was going to food delivery and restaurants almost every night of the week. Forgotten subscriptions. A pattern of upgraded gear for the kids' activities every season. Nothing outrageous in isolation. But added up, it was a pretty clear picture.

When I asked them what they wanted most in life, they said time. Security. A real vacation without rushing back. They talked about wanting to slow down before the kids got older and stopped wanting to hang out with them.

The spending wasn't writing that story.

That's not a math problem. It's an alignment problem, a gap between the values they'd state out loud and the values their checking account had quietly adopted.

The Story I Wasn't Ready to See

I've been on the other side of this too.

When the triplets were born, and I was still deep in corporate life, I kept spending like the person I used to be. Tech gear for hobbies I no longer had time for. Things that fit a version of myself I'd already left behind. Meanwhile, Theresa and I were cutting corners on things that would have actually helped. The kind of support that gave you any margin when you have three newborns and a house and a career that doesn't pause.

My spending was writing an old story. One that hadn't caught up to the life we were actually living.

It took a while to see it. Honestly, it took someone outside my own head to point it out.

Inherited Spending Patterns

Here's something I see constantly in my generational practice at TAMMA.

Financial behaviors are passed down. Not always intentionally. But a client's adult child comes to talk with me, and they often show the same spending patterns as their parents. The same anxieties. The same places where money flows without question. The same spots where they feel guilty spending even when it makes sense.

They didn't consciously decide to adopt those patterns. They absorbed them. The art of spending, in many families, is actually inherited, handed down like a piece of furniture nobody questioned because it's always been there.

Part of the work I do with families is helping them see which patterns they chose and which ones chose them. That distinction matters more than any spending category.

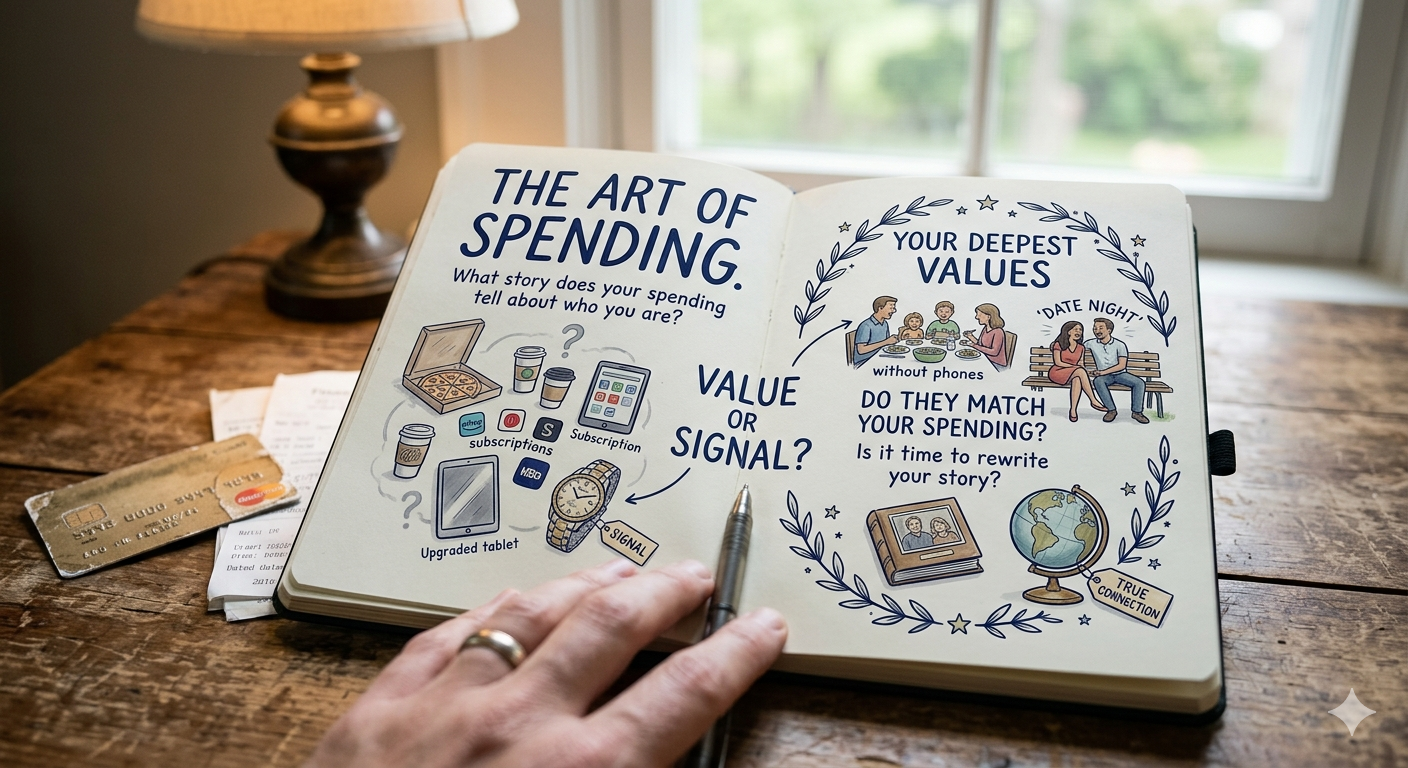

The Signal vs. the Value

There's a question I've started asking clients when we go through spending together: is this a value, or is it a signal?

Some spending reflects something you genuinely care about. You spend on your kids' activities because you want them to develop discipline, skills, and team experience. You spend on date nights because that relationship is the foundation for everything else.

But some spending is a signal. It's meant to communicate something to yourself, to your neighborhood, to your social circle. I'm doing fine. I belong here. I'm the kind of person who has this.

Neither one is inherently wrong. But they're different, and they deserve different questions.

If you've never stopped to separate the two, you may be directing significant money toward a story you never consciously chose.

One Small Thing

I don't want to make this sound heavier than it is.

This isn't about guilt. It's not about judging your latte, your vacation, or your kids' gear. Busy parents have enough guilt already.

It's about clarity.

Because for most of the families I work with, the financial breakthrough doesn't come from finding a better investment. It comes from finally seeing what their money has been saying about them all along and deciding whether that's the story they want to keep telling.

Before your next few purchases this week, anything over $20, pause for 5 seconds and ask: does this reflect what I actually value, or what I'm trying to signal?

You don't need to change anything. Not yet. Just notice.

Because once you can see the story you're spending is telling, you get to decide whether it's the story you actually want to write.

Money is a number. Enough is a story. Make sure you're writing your own.